{kind=link}

For most of the past century, a green-and-yellow tractor rolling across a commercial farm anywhere from the Free State to the Rift Valley has meant one thing: John Deere.

The American manufacturer built its African reputation the same way it built its global one — on durability, resale value, and a dealer network that could get a broken combine back into a field before a harvest window closed. That reputation still counts for a great deal. But it is no longer the whole story.

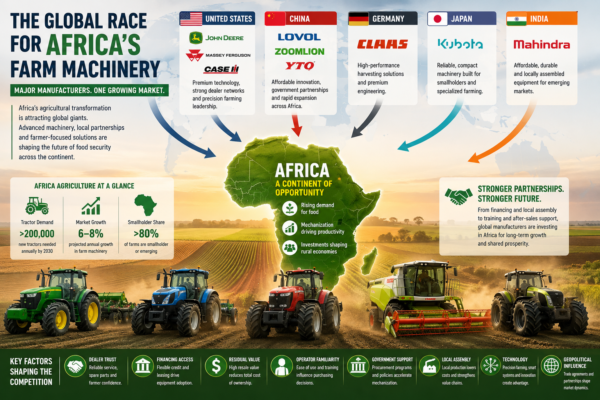

Africa has quietly become the most contested frontier in global farm equipment. A wave of manufacturers — from AGCO’s Massey Ferguson and Fendt brands to CNH Industrial’s Case IH and New Holland, from Japan’s Kubota to India’s Mahindra, and a fast-growing cohort of Chinese entrants led by Lovol, Zoomlion and YTO — are converging on the continent at the same moment that population growth, food-security anxiety, commercial farming expansion and government mechanization programmes are pushing demand for tractors and harvesters higher than at any point in Africa’s history.

The Africa agricultural tractor machinery market alone was worth an estimated $2.36 billion in 2025 and is forecast to climb toward $3.26 billion by 2031, while the broader agricultural machinery market on the continent is projected to reach roughly $6.3 billion by 2030.

What is unfolding is not a simple two-way contest between an American incumbent and a set of challengers.

It is a layered competition across price tiers, technology levels and geography — European and American premium brands defending share in commercial farming belts, Japanese and Indian manufacturers fighting for the mid-market and smallholder segments, and Chinese state-linked and private groups undercutting almost everyone on price while investing heavily in local parts warehouses and service networks.

For African farmers, dealers, policymakers and investors, understanding how these companies are positioning themselves is no longer a niche industrial question. It is central to how the continent mechanizes.

Why Africa Has Become the World’s Next Machinery Battleground

The numbers explain the rush. Sub-Saharan Africa averages fewer than two tractors per 1,000 hectares of arable land, compared with roughly 200 tractors per 1,000 hectares across the United States and Europe — a gap of two orders of magnitude that has persisted for decades despite repeated mechanization drives.

Some regional analyses put the sub-Saharan average slightly higher, around 28 tractors per 1,000 hectares, but even that more generous figure is a small fraction of global norms.

Either way, the conclusion is the same: Africa is mechanized at a level that no longer matches its population, its food-import bill, or its ambitions for commercial agriculture.

That gap is now closing, unevenly but visibly. Kenya’s tractor market is expanding at close to 8% a year as county governments subsidize mechanization to support food-security targets.

Nigeria has just launched what its agriculture ministry describes as the largest single mechanization programme on the continent — 2,000 heavy-capacity tractors and more than 9,000 implements being distributed in phases to mechanization service providers under a lease-to-own model, backed by financing from the Bank of Agriculture.

South Africa’s tractor sales rose nearly 19% in 2025 over the prior year, and January 2026 sales figures came in well ahead of the same month a year earlier, reflecting renewed farmer confidence after several difficult seasons.

Ghana has signed a deal with Turkish manufacturer Hattat Traktör to establish local assembly. Ethiopia, which placed a headline-making $100 million tractor order with China’s YTO Group back in 2013, remains one of the continent’s most closely watched government-driven mechanization markets.

Behind these individual moves sits a broader structural shift. Commercial farm operations are consolidating and scaling up in several markets, creating demand for higher-horsepower equipment more typical of European and American row-crop operations.

Governments across the continent — from Nigeria’s federal mechanization scheme to Kenya’s county-level tractor-hire subsidies — are treating mechanization as a food-security instrument rather than a purely commercial one.

Digital tractor-hire platforms, most notably Nairobi-based Hello Tractor, are lowering the effective cost of access for smallholders who could never justify outright ownership, converting latent demand into real transactions.

And completely knocked-down (CKD) assembly is spreading from South Africa and Kenya into markets like Tanzania, Zambia and Ethiopia, letting manufacturers sidestep import duties and currency risk while building local employment goodwill with host governments.

Financing remains the connective tissue holding all of this together. Loan caps and foreign-currency shortages continue to limit outright purchasing power in Nigeria and several other markets, which is precisely why manufacturers offering mid-tier, lower-priced equipment — Mahindra and Kubota chief among them — have been gaining ground even against better-known premium names.

John Deere: The Benchmark Everyone Else Is Measured Against

John Deere’s position in Africa was not inherited; it was built. Through its Africa and Middle East regional structure, the company has spent decades layering a dealer and parts network across the continent’s commercial farming belts — South Africa, Zambia, Kenya, and increasingly West Africa — that competitors still cite as the standard to beat.

Deere’s brand equity rests on three pillars: engineering reliability suited to punishing conditions, strong resale value that lowers the effective cost of ownership over a machine’s life, and a precision-agriculture ecosystem — GPS guidance, telematics, data-driven farm management — that increasingly matters to the continent’s larger commercial operations.

That technology push has extended into unconventional territory. In one of its more telling African moves, Deere took a minority stake in Hello Tractor, the Kenyan-founded tractor-sharing platform, explicitly to learn how a mechanization model built for fragmented smallholder plots — rather than the large contiguous farms Deere’s core business was designed around — actually works.

Deere’s Africa and Asia sales leadership has described the deal as part of a broader ambition to have effectively all of its small agricultural equipment connectivity-enabled, and as a way to understand customer needs in markets where the standard American or European ownership model does not translate cleanly.

Deere’s challenge in Africa is not product quality; it is positioning. The company’s core strength is in mid-to-large commercial operations that can absorb premium pricing and benefit from full-service dealer support.

That leaves it structurally exposed at the lower end of the market, where cost sensitivity dominates purchasing decisions and where Chinese and Indian manufacturers have built their entire African strategies around undercutting exactly that price ceiling.

Deere’s dealer network, while strong in South Africa and pockets of East and Southern Africa, also thins noticeably the further one moves into West and Central Africa — precisely the regions where population growth and mechanization programmes are creating the fastest-growing pools of new buyers.

The Main Challengers

AGCO: Massey Ferguson and Fendt

Massey Ferguson is arguably the single most recognized tractor brand across Africa, a status built over generations rather than years.

AGCO, its parent company, has pursued what it calls a three-segment tractor strategy for Africa and the Middle East — offering an entry-level range alongside its established mid-tier and premium global series, so that farmers at very different stages of mechanization can stay within the same brand as their operations grow.

That tiered approach, combined with assembly and distribution footprints in markets including Nigeria, South Africa, Algeria and Zimbabwe, has kept Massey Ferguson competitive against both premium Western rivals and lower-cost Asian entrants simultaneously.

AGCO’s Fendt brand occupies a different lane entirely — a premium, technology-forward line aimed at the continent’s largest and most sophisticated commercial farms, where AGCO is increasingly bundling automation, telematics and retrofit precision-agriculture tools around the hardware rather than competing on horsepower alone.

That combination — a value brand for scaling smallholders and a premium brand for elite commercial operations — gives AGCO a wider addressable market in Africa than almost any single competitor, John Deere included.

CNH Industrial: Case IH and New Holland

CNH Industrial’s two African-facing brands split the market along familiar commercial and mixed-farming lines.

Case IH is positioned toward large-scale commercial grain and row-crop operations, where its combine harvesters compete directly with John Deere’s and CLAAS’s flagship machines — South African revenue data from recent years put Case IH’s local combine-harvester sales ahead of several rivals, a signal of real commercial-farming traction rather than niche presence.

New Holland, meanwhile, has built a broader footprint across mixed farming operations and has historically been a strong performer in South Africa’s combine-harvester segment as well.

Both brands have leaned into precision farming as a differentiator, but CNH’s African strategy has been less about flashy new-market entry and more about defending entrenched commercial-farming relationships in South Africa, and to a lesser extent Kenya and Zambia, while relying on regional distributor networks rather than large-scale local assembly to reach the rest of the continent.

Kubota

Kubota’s African story is one of a slow, deliberate correction. The Japanese manufacturer entered the continent in 2017 through a Kenyan subsidiary but struggled for years against a fundamental problem: its tractors, built to Japanese engineering and cost standards, were priced above what most African smallholders and mid-tier commercial farmers could justify.

Kubota’s 2022 acquisition of India’s Escorts Limited — owner of the Farmtrac and Powertrac brands already well established in Nigeria, Angola, Burkina Faso, Egypt and Tanzania — was a direct response to that pricing mismatch, giving Kubota a lower-cost product line manufactured to Indian cost structures roughly 30% below Japanese equivalents.

That strategy is now accelerating. Kubota has signed a financing partnership with Sumitomo Mitsui Banking Corporation specifically to boost farm-machinery sales in Africa and is targeting roughly 4,000 tractor shipments a year to the continent by 2030 — five times its recent volumes.

Its compact and mid-horsepower models remain particularly well suited to horticulture and rice farming in markets like Madagascar, Senegal and Uganda, and to the smallholder segment more broadly, where Kubota’s reputation for engine longevity and mechanical simplicity carries real weight even among buyers who have never purchased new equipment before.

Mahindra

Mahindra & Mahindra holds a title that surprises people outside the industry: by volume, it is the world’s largest tractor manufacturer, and its African ambitions match that scale.

Rather than relying purely on imports, Mahindra has built or planned local assembly operations across an unusually wide spread of countries — Kenya, Tanzania, Algeria, Tunisia, Mali, Chad and others — explicitly framing local assembly as both a cost advantage and a way to customize machines for local terrain and crop conditions.

Company executives have been candid that Mahindra’s approach differs from many Indian and Chinese competitors who chase bulk government deals; instead, Mahindra has prioritized building durable retail distribution relationships, such as its partnership with Simba Colt Aspire in Kenya to distribute a range spanning 25 HP to 92 HP models aimed squarely at the country’s smallholder base.

Affordability remains Mahindra’s core weapon, but it is reliability and fuel efficiency — not just sticker price — that dealers and farmers most often cite when explaining the brand’s growing following in Kenya, Zambia, Mozambique and South Africa.

That combination has made Mahindra one of the few manufacturers credibly competing across both the smallholder and lower-commercial segments at once.

Lovol

Of the Chinese manufacturers pushing into Africa, Weichai Lovol has arguably built the most comprehensive playbook.

Lovol’s African strategy rests on three legs: a genuinely broad product range running from compact models suited to smallholder plots up to high-horsepower units like its TD1304, deployed on large-scale farms in Angola, Ethiopia and Zambia; aggressive participation in government-to-government cooperation forums, including donating tractors at cooperation summits with countries like Mali; and — critically — investment in localized after-sales infrastructure that most Chinese competitors have historically neglected.

Lovol’s newly opened parts warehouse in Zimbabwe, offering round-the-clock parts supply, is a direct answer to the most common criticism leveled at Chinese equipment in Africa: that machines are cheap to buy but expensive and slow to keep running once something breaks.

Lovol has also pushed into technology areas historically dominated by Western brands, including continuously variable transmission (CVT) high-horsepower tractors, a segment where it claims to be the first Chinese manufacturer to commercialize the technology domestically before exporting it.

Its harvesting equipment — including wheeled and crawler harvesters serving Nigeria and Ghana’s rice sector — has found real traction in crop segments that many premium Western brands have historically underserved.

Building trust in African markets increasingly depends on after-sales support rather than purchase price alone. Chinese manufacturers have recognised that long-term success requires investing in local service capabilities alongside machinery sales.

“We have built sales and service networks across multiple countries and trained local technicians to ensure the equipment can operate reliably and be easily maintained,” said Zhang Qi, Sales Manager at Shandong Shonly Modern Agricultural Equipment Co., Ltd. “Meanwhile, we also tailor our products to local conditions.”

Zoomlion

Zoomlion arrived in African agriculture from an adjacent industry — construction and mining equipment, where the Chinese group already had an established footprint in South Africa — and is now using that beachhead to expand aggressively into farm machinery.

Its pitch is explicit: bringing what it calls first-world technology at meaningfully lower prices than established Western brands.

At South Africa’s NAMPO Harvest Day in 2026, Zoomlion showcased its DV3504 hybrid tractor, which it describes as a commercial first for the market, alongside the DQ2604, both aimed at large-scale farming applications where fuel costs are a significant operating expense.

Zoomlion‘s after-sales commitments are notably aggressive for a relatively new entrant: a standard two-year or 2,000-hour factory warranty, extending up to five years on machines fitted with high-performance lithium battery systems, plus a pledge of 24-hour parts delivery or a substitute machine while repairs are carried out — language clearly designed to counter skepticism about Chinese equipment support.

The company already describes an established agricultural-machinery footprint in China, Turkey, Russia, Australia, Kenya and Tanzania, and frames South Africa explicitly as a stepping stone into the wider Southern African Development Community market rather than an endpoint.

YTO Group

YTO Group, manufacturer of the historic Dongfanghong (“The East Is Red”) tractor brand and part of state-owned conglomerate Sinomach, is China’s largest tractor producer by volume, with a factory floor in Luoyang reportedly completing a new tractor roughly every three minutes.

Its African relationship is older and more government-driven than most Chinese competitors’: the 2013 sale of $100 million worth of tractors to Ethiopia remains one of the largest single agricultural equipment transactions on the continent and established YTO as a serious state-to-state supplier rather than a purely commercial brand.

YTO has since built out authorized export partners and regional service infrastructure — including some of the first Chinese-operated overseas spare-parts centers established in Vietnam and Nigeria — to support growing sales in Nigeria, Kenya and South Africa.

Its pitch leans less on cutting-edge precision technology than on production scale, price and the political relationships that come with operating as an arm of Chinese state industrial policy, a combination that has proven durable in markets where government procurement and bilateral cooperation agreements shape a meaningful share of large equipment purchases.

CLAAS

CLAAS occupies a narrower but well-defended niche: high-end harvesting equipment. The German family-owned manufacturer, the European market leader in combine harvesters and widely regarded as the global leader in self-propelled forage harvesters, has built its African presence through a mix of direct dealer development and imports rather than large-scale local assembly.

Its LEXION and TRION combine series compete directly with John Deere and Case IH at the premium end of South Africa’s harvesting market, and 2020 revenue data for CLAAS’s South African combine business suggests real commercial-farming penetration, even if it trails the largest American players in absolute scale.

CLAAS’s African expansion has proceeded through what the company itself describes as collaborations and pilot projects designed to extend German engineering quality into markets with less mature dealer infrastructure — a slower, more deliberate approach than the volume-driven strategies of its Chinese rivals, but one consistent with CLAAS’s global reputation for precision engineering over price competition.

The Wider Field of Chinese Entrants

Beyond Lovol, Zoomlion and YTO, a broader wave of Chinese manufacturers is entering Africa’s tractor, sprayer, forage-equipment and implement segments, often through trading-company intermediaries rather than direct subsidiaries.

Turkey’s Hattat Traktör, while not Chinese, belongs to this same emerging cohort of non-traditional entrants using government-to-government assembly deals — its recent Ghana agreement is a clear example — to establish beachheads that larger, more established brands have been slower to pursue.

What unites this wider field is a shared recognition that price sensitivity, not brand prestige, is currently the dominant purchasing factor across most of Africa’s mechanization pipeline, and that whoever solves the parts-and-service problem at scale, rather than simply undercutting on sticker price, stands to capture the most durable share.

Beyond price, Chinese manufacturers are increasingly positioning themselves as practical partners for Africa’s mechanization drive.

Industry observers note that many African farmers are prioritizing reliability, affordability and ease of maintenance over premium technologies that often remain out of reach for smaller commercial operations.

“Chinese machinery offers high performance at competitive prices, allowing modernization without breaking the bank,” says Soukaina Homaid, a Moroccan trade and agricultural industry expert.

“These affordable, practical tools are particularly well suited to African smallholders who prioritize simplicity, reliability and accessibility over unnecessary technological complexity.”

The Technology Race

Precision agriculture — GPS guidance, automated steering, telematics-based fleet monitoring and increasingly autonomous field operations — has become the primary battleground among the premium brands, with John Deere, AGCO and CNH Industrial all racing to extend data-driven farming tools into African commercial operations large enough to benefit from them.

But the more consequential technology contest for the continent as a whole may be happening at the Chinese end of the market.

Both Lovol and Zoomlion have moved aggressively into hybrid and electric-drive machinery — Zoomlion’s DV3504 hybrid tractor and Lovol’s CVT high-horsepower line are explicit attempts to leapfrog directly into next-generation drivetrains rather than competing purely on conventional diesel specifications, betting that fuel costs and emissions pressure will make hybrid and electric machinery commercially relevant in Africa sooner than incumbents expect.

This creates an unusual dynamic: African buyers, particularly larger commercial operations, are increasingly being offered genuinely current-generation technology from Chinese manufacturers at price points well below Western equivalents, rather than the previous generation of Western technology at a discount.

Whether that technology proves as durable and serviceable as the established Western and Japanese equipment it is displacing remains the open question shaping purchasing decisions across the continent.

Dealer Networks and After-Sales Support: The Real Battleground

Ask any experienced African equipment dealer what actually decides a tractor sale, and horsepower rarely tops the list.

Service turnaround, spare-parts availability, technician training and financing terms consistently matter more, because a machine sitting idle during planting or harvest season costs a farmer far more than the price difference between competing brands.

Industry data suggests the best-served commercial farming corridors — where major manufacturers maintain training academies and parts depots — keep machine availability above 92%, a figure that drops sharply in less-served regions.

This is precisely why the recent moves by Chinese manufacturers to open localized parts warehouses — Lovol’s Zimbabwe facility being a clear example — matter more than they might appear at first glance.

For years, the principal argument against Chinese equipment in Africa was not price or build quality but the fear of being stranded without parts or service.

Manufacturers that solve that problem credibly are positioned to convert price advantage into durable market share rather than one-off bargain sales.

Established players like John Deere, Massey Ferguson and Kubota, meanwhile, are defending their positions by deepening rather than merely maintaining their dealer networks — extending technician training programmes and, in Kubota’s case, pairing expansion with dedicated financing partnerships to lower the barrier to first purchase.

Who Offers the Best Value?

There is no single answer, because “value” means different things to a two-hectare horticulture farmer in Uganda and a 2,000-hectare grain operation in the Free State.

On purchase price alone, Chinese brands led by Lovol, Zoomlion and YTO, alongside Mahindra’s entry-level range, sit well below Western and Japanese equivalents.

On fuel efficiency and total lifetime maintenance cost, Kubota and Mahindra’s compact and mid-horsepower lines have built strong reputations for low running costs, particularly on smaller plots where big, powerful machines are inefficient regardless of brand.

On resale value and durability over a long ownership horizon, John Deere and Massey Ferguson retain a meaningful edge, reflecting both engineering reputation and the depth of their secondary markets.

On warranty terms, Zoomlion’s aggressive two-to-five-year commitments currently outpace most rivals on paper, though the brand’s track record over a full equipment lifecycle in Africa is still relatively short.

On harvesting technology specifically, CLAAS, John Deere and Case IH remain the reference points for large commercial operations, with Chinese and Indian entrants still working to establish comparable credibility in that segment.

What African Farmers Should Consider

Farm size and crop type should drive the horsepower and implement decision before brand does — a compact Kubota or entry-level Mahindra suits a smallholder horticulture operation far better than a high-horsepower unit designed for row-crop grain farming, regardless of price.

Terrain matters just as much: hilly, fragmented smallholder plots common across much of East and Central Africa favor compact, maneuverable machines over the large four-wheel-drive units that dominate South Africa’s flatter commercial farmland.

Financing availability often narrows the realistic choice set more than preference does, particularly in markets with tight loan caps or foreign-currency constraints, which is part of why mid-tier Indian and Japanese brands have gained ground even where farmers might otherwise prefer a premium Western machine.

Finally, buyers should weigh long-term ownership costs — parts availability, technician access, and resale value — as heavily as sticker price, since the cheapest tractor to buy is not always the cheapest to own over a full working life.

China’s growing influence in Africa’s agricultural machinery sector is being reinforced not only by manufacturing capacity and competitive pricing but also by evolving trade policy.

Beijing’s decision to introduce a 100% zero-tariff policy on imports from eligible African countries between May 2026 and April 2028 is expected to deepen two-way trade and strengthen industrial cooperation.

While the policy directly targets African exports entering China, economists believe it also encourages broader commercial partnerships, investment and equipment trade between Chinese manufacturers and African markets.

For agricultural machinery companies, the policy comes at a time when many African governments are accelerating mechanization programmes to improve food security, reduce dependence on food imports and increase agricultural productivity.

Economic experts argue that China’s newly implemented zero-tariff initiative could strengthen reciprocal trade and encourage greater investment in agricultural mechanization, supporting Africa’s long-term food security ambitions.

| Manufacturer | Country | Strength | African Strategy |

|---|---|---|---|

| John Deere | USA | Premium technology | Dealer network |

| Massey Ferguson | USA/AGCO | Versatility | Multi-segment |

| Case IH | USA/CNH | Commercial farms | Precision farming |

| Kubota | Japan | Small tractors | Smallholder focus |

| Mahindra | India | Affordability | Local assembly |

| Lovol | China | Value & innovation | Government partnerships |

| Zoomlion | China | Hybrid tractors | Smart farming |

| YTO | China | Large production | State cooperation |

| CLAAS | Germany | Harvesting | Premium combines |

Will Chinese Brands Overtake John Deere in Africa?

For decades, John Deere has occupied an enviable position in African agriculture. Its machines have earned a reputation for durability, reliability and strong resale values, particularly among commercial farmers who depend on equipment that can withstand demanding operating conditions.

Yet the competitive landscape is changing rapidly. Chinese manufacturers such as Lovol, Zoomlion and YTO are no longer competing solely on price. They are investing in technology, local partnerships and after-sales support with the clear ambition of becoming long-term players in Africa’s mechanization journey.

Whether they can eventually overtake John Deere will depend on far more than horsepower or purchase price.

Dealer Trust Remains John Deere’s Greatest Asset

One of John Deere’s biggest competitive advantages is not its tractors—it is its dealer network.

Across major farming regions in South Africa, Kenya, Zambia and parts of West Africa, farmers know they can access trained technicians, genuine spare parts and warranty support when machinery breaks down.

During planting or harvest, every hour of downtime can translate into significant financial losses, making dependable service infrastructure one of the most important purchasing considerations.

Chinese manufacturers have recognised this weakness in their historical business model and are responding aggressively. Companies including Lovol and Zoomlion have begun establishing regional spare-parts warehouses, expanding dealership networks and training local technicians to improve customer confidence.

“We have built sales and service networks across multiple countries and trained local technicians to ensure the equipment can operate reliably and be easily maintained,” said Zhang Qi, Sales Manager of Shandong Shonly Modern Agricultural Equipment Co., Ltd. “Meanwhile, we also tailor our products to local conditions.”

While these investments are narrowing the service gap, dealer confidence is built over decades rather than years. John Deere continues to enjoy a considerable first-mover advantage in this area.

Financing Is Becoming the New Competitive Weapon

Access to finance increasingly determines which machinery reaches African farms.

Many farmers struggle to secure affordable credit for premium equipment, making total acquisition cost just as important as machine performance. Chinese manufacturers often benefit from export financing, state-backed credit facilities and flexible payment structures that reduce barriers to ownership.

Several governments have also negotiated machinery supply agreements directly with Chinese manufacturers through broader economic cooperation programmes, making Chinese equipment more accessible than many Western alternatives.

At the same time, established manufacturers are strengthening their own financing offerings. Kubota, Mahindra, AGCO and CNH Industrial have expanded partnerships with commercial banks, development finance institutions and equipment leasing companies to make mechanization more affordable.

The competition is increasingly shifting from selling tractors to financing agricultural transformation.

Residual Value Still Favours Premium Brands

Although Chinese machinery has improved significantly in quality over the past decade, resale value remains one of John Deere’s strongest advantages.

Used John Deere tractors consistently command premium prices across African markets because buyers trust the brand’s long-term reliability, parts availability and dealer support. Strong residual values effectively reduce the total cost of ownership, allowing commercial farmers to recover a larger portion of their initial investment when upgrading equipment.

Chinese brands are gradually improving their reputation, but developing a robust second-hand market requires years of proven field performance. Until that confidence matures, John Deere and other established manufacturers are likely to maintain an important advantage.

Operator Familiarity Shapes Purchasing Decisions

Farmers tend to buy what they know.

Generations of African operators have been trained on John Deere, Massey Ferguson, New Holland and Case IH equipment. Mechanics are familiar with these machines, spare parts are widely available and operators understand their maintenance requirements.

Chinese manufacturers are addressing this challenge by simplifying machine operation, translating technical documentation into local languages and offering operator training alongside equipment sales.

Their focus on practical, user-friendly machinery is resonating with many first-time buyers.

“Chinese machinery offers high performance at competitive prices, allowing modernization without breaking the bank,” says Soukaina Homaid, a Moroccan trade and agricultural industry expert. “These affordable, practical tools are ideal for African smallholders prioritizing simplicity over high-tech complexity.”

For many emerging farmers, ease of use and affordability outweigh premium features they may never fully utilise.

Government Procurement Is Accelerating China’s Expansion

Government purchasing programmes have become one of China’s most powerful routes into African markets.

Across the continent, mechanization initiatives aimed at improving food security increasingly rely on bilateral cooperation agreements that include tractors, harvesting equipment and agricultural implements supplied by Chinese manufacturers.

Large public procurement programmes in countries such as Ethiopia, Nigeria and several West African nations have significantly expanded the visibility of Chinese brands while creating opportunities for dealer development and local service infrastructure.

Government-backed projects also provide manufacturers with immediate fleet deployments, allowing machines to demonstrate performance under local operating conditions.

Local Assembly Is Changing the Economics

Rather than relying exclusively on imports, manufacturers are increasingly establishing assembly operations within Africa.

Local assembly reduces import duties, shortens delivery times, lowers transportation costs and creates local employment opportunities. Governments frequently encourage these investments through incentives designed to strengthen domestic manufacturing capabilities.

Indian manufacturers such as Mahindra have embraced this model for years, while Chinese companies are increasingly exploring assembly partnerships as demand grows.

For African governments, local assembly offers political and economic benefits that extend well beyond agriculture, making it an increasingly important factor in procurement decisions.

Technology Leadership Is No Longer Exclusive to Western Brands

For many years, precision agriculture represented a clear advantage for John Deere and other Western manufacturers.

GPS-guided steering, telematics, autonomous operation and digital farm management systems became defining characteristics of premium machinery.

Today, however, Chinese manufacturers are investing heavily in hybrid drivetrains, smart farming platforms, automation and artificial intelligence.

Zoomlion’s hybrid tractors and Lovol’s high-horsepower continuously variable transmission (CVT) models illustrate how Chinese manufacturers are attempting to leapfrog traditional development pathways rather than simply replicating older Western technologies.

The technology gap has narrowed considerably, although questions surrounding long-term durability, software support and lifecycle performance remain under evaluation by many commercial operators.

Geopolitical Influence Is Reshaping the Market

Competition between machinery manufacturers is increasingly intertwined with international trade and diplomacy.

China’s growing economic engagement across Africa—including infrastructure investment, industrial cooperation and agricultural partnerships—has strengthened commercial relationships that naturally support machinery exports.

The country’s recently introduced 100% zero-tariff policy on eligible African imports, running from May 2026 through April 2028, is expected to deepen two-way trade and encourage broader industrial cooperation.

Economic analysts argue that the initiative could stimulate investment in agricultural modernization while reinforcing mechanization as a cornerstone of Africa’s long-term food security strategy.

Western manufacturers continue to enjoy strong brand recognition and technological leadership, but Chinese companies increasingly benefit from integrated trade, financing and development initiatives that extend well beyond equipment sales.

The Verdict

Will Chinese brands overtake John Deere in Africa?

The answer is not yet—but the gap is narrowing faster than many expected.

John Deere still leads where it matters most to established commercial farmers: dealer confidence, resale value, proven reliability and a mature service ecosystem. Those advantages cannot be replicated overnight.

However, Chinese manufacturers are transforming from low-cost alternatives into credible global competitors. Competitive pricing, improving product quality, expanding dealer networks, localized assembly, flexible financing and sustained government partnerships are creating a compelling value proposition for many African buyers.

The future of Africa’s agricultural machinery market is therefore unlikely to belong to a single dominant manufacturer.

Instead, it will be defined by intensifying competition in which farmers benefit from greater choice, faster technological innovation and more accessible mechanization solutions.

For John Deere, maintaining leadership will increasingly depend not only on engineering excellence but also on adapting to an African market where affordability, localized support and strategic partnerships are becoming just as important as horsepower.

Also Read

- Ghana Orders 1,840 Belarusian Farm Machines in Major Push to Modernize Agriculture

- Nigeria Scraps All Import Duties on Farm Machinery in Biggest Tariff Overhaul in Years

- Tractor Prices May Be About to Shift — Here’s What Farmers and Buyers Need to Know

- Mahindra Cuts Ties with Mitsubishi — Then Bets Big on North America

Martin is a writer at Agrimachinery Africa specializing in agricultural machinery, mechanization trends, and farm technology across Africa. His work focuses on tractors, harvesting equipment, irrigation systems, and emerging innovations helping farmers improve productivity and efficiency. Through in-depth industry coverage, he highlights technologies shaping the future of modern agriculture.